Paul Graham says decide to invest within 24 hours! Evidence says do at least 40 hours of due diligence!

Have you read the latest essay from Paul Graham, founder of Y Combinator?

The premise of investing within 24 hours clearly has some merit but, I think it remains out of reach for most Angel investors. It can work for those who are very, very rich and those who live deep in the heart of their investment domain – like Paul. Most of us cannot afford to invest a million dollars a week, or even a month on a sustained basis and that is what 24 hour decisions for $100,000 investments means. Of course, the upside is you can get all your investing done in a few weeks and can spend the rest of the year on the beach/couch/hammock/whatever reflecting on how easy it is to lose large amounts of money quickly.

Will the venture capital game change?

Paul’s focus in his essay is venture capital (VC) and some of his observations are well known to us. Will the VC model change? – yes, undoubtedly. Is it true that founders don’t need money as badly as they once did – not so sure but, I accept that they can need less. That has been true and more readily apparent for many years to those of us who operate outside the overblown egos and large fund sizes of Silicon Valley.

Such harsh words, for such glowing figures?

To be honest, I’m not entirely sure how to understand his reference to investors being “founders’ bitches” but, certainly he is right that micromanaging founders is not and, frankly, never has been a sound investment approach. I think, as investors, we need to know more about more than our founders but, that doesn’t mean we know the right answers all the time.

To me it is more about process and strategy, our ability to see ahead to the pot holes in the road and the opportunities that might arise. We offer not only early-warning but, possible strategies for taking advantage of opportunities or for ameliorating the damage done in crossing the inevitable rough patch. Ultimately, though, it is up to the founders to make the decisions and take the actions.

The ‘Golden Rolodex’

A pivotal aspect of the Y Combinator value and success has been the ‘Golden Rolodex’. Initially Paul’s and later from other mentors in the team too. The ability to shoehorn promising young ventures into a seat in front of the very best investors and the right corporate partners is an enormous advantage. Many Angel investors offer the same benefit to their portfolio companies, albeit in differing market sectors and geographies.

The valuation discussion remains distorted because Paul paints a picture of a VC focused only on a percentage correlated to the amount they must deploy to meet their objectives as fund managers. As Angels we know that the real discussion is not about the amount of money per se but, about the future, the likely growth of the business and the bigger that potential, the more valuable our contribution is at the earliest stage.

Hey, which way to the exit?

Focusing on exit – and particularly, a strategic exit – rallies the thinking around valuation on the value of the investor not the investment. Founders who want dumb money are increasingly able to get it quickly and at a lower cost. Founders who want smart money will recognise that smart, also requires a little more deliberation which, in the end, will deliver greater value and higher growth multiples to fuel a large exit.

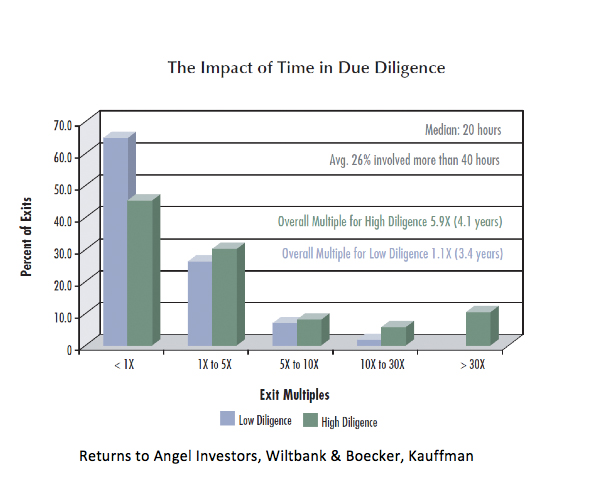

For my part, while I prefer faster decisions than the months it takes to get a group across the line I also value, the many times when a little delay has afforded me the opportunity to see the flaws in a deal and avoid losing my money in an unwise investment. Indeed, research into Angel investing has shown a strong correlation between returns and effort in due diligence with the best returns being achieved for investments that complete at least 40 hours of due diligence. So, the evidence would tend to suggest that Paul’s proposition, at least for Angels, is inappropriate.

Speed is a matter of context

In most parts of the world Paul’s six weeks to raise capital is more like six months, or longer. The folks in Silicon Valley always sneer at such time frames and thus, teach even our local entrepreneurs to frown on that pace. Yet, without the intensity and depth of the Silicon Valley market it is not practical for early-stage investors or founders to act as if they are in Silicon Valley. Indeed, if we are not in Silicon Valley we probably don’t face the sort of competition for deal flow that Paul assumes and, for Angels, unlike VC, we don’t have to do a deal at all.

VC have a contract to invest someone else’s money and to get it put to work within a very limited time frame – quite literally they must consume all their capital. In comparison, Angels are beholden only to themselves (and perhaps a spouse) and, as such, are not interested in consuming all of their capital at breakneck speed. If Angels don’t like the shape of a deal or the way the process is being handled – and yes, that can mean if it is not according to the Angel’s rules – then we don’t have to invest at all. After all, Angels aren’t making a living from their investments and in most deals they lose all of their money so, some patience and process certainly seem prudent.

Embrace the angels

I encourage entrepreneurs to develop relationships with the Angels well before the venture needs capital. That helps shorten the decision cycle and also makes for a better decision by both parties. One of the most important aspects for founders and one not often contemplated in narratives like Paul’s, is that founders are the ones making the key decision not investors. Founders are deciding which investors to take on-board and in so doing are making one of the most pivotal decisions for the future of their venture. Bad investors are far worse than bad employees. You can fire the latter but, the former remain a problem and often a fatal infection for the venture.

People tend to be consistent, as Paul points out when he describes the risk profile of investors. So an investor who decides within 24 hours on making an investment with the obviously limited information and time for consideration that that implies is very likely to make all decisions that same way throughout the life of the company. That encourages a dynamic in which the entrepreneur is even more highly motivated to withhold information if they think it will produce an ill-considered response from investors, a rapid decision that will damage the business.

Ultimately, founders and investors both want to make decisions expeditiously so that the business can keep pace with the market and take best advantage of all opportunities but, that demands a degree of consideration and deliberation. As the business gets more complex, more mature, more dynamic the time required for obtaining, absorbing and responding to all the relevant information increases. To preserve short decision-making cycles large companies employ teams and systems not readily available to early-stage ventures and, even if they were, start-up entrepreneurs are rarely skilled in using such systems.

Communicate with the angels…

This is precisely where the value of the investor can be most apparent. A founder who keeps his Angel investor well informed can leverage the experience of the investor to help make expeditious but, well considered decisions. Of course, that only works if the investor has the experience, thus, a 24 hour commitment cycle is not enough time for the founder to really know if the investor has anything more than money to offer.

Paul suggests that “few investors understand the cost that raising money from them imposes on startups”.

Really?

In the angel world, most of the investors have been there, done that and often more than once. Indeed, it is because Angels understand only too well the impact of fundraising that we tend to agonise over ways to deliver value to every founder at every engagement whether we have decided to invest yet or not. I am sure that Paul is not naïve so I can only assume he has the VC investors in mind but, even then, I really doubt that any of the quality general partners are so naïve either.

I can only conclude that Paul is referring to the expanding bubble of johnny-come-lately investors we see in every bubble cycle, the people who have little more than money to offer and are attracted by the recent front page news success stories without understanding what it takes to help those companies succeed.

The quality of the entrepreneur

So we come to another of Paul’s observations, the quality of the entrepreneur. As more and more people start new companies in the hope of fame and riches it is harder and harder to find the individuals with a real vision about changing the world. That rhetoric of the VC investor and the Angel remains a strong and effective bias. When asked what makes the A-grade team we are all looking to back the vast majority of early-stage investors still refer to the vision and passion of the founders for a new world. Yes, we want founders who expect to create substantial value and then sell it so that together they and their investors can reap the financial rewards. However, too many of the newly minted entrepreneurs these days are chasing only the money and have no real or credible vision to change the world.

On the other side of the table there are an increasing number of people trying to be early-stage investors and they too lack experience, expertise and capability. Organised Angel communities offer training, collaboration and professional process to help early-stage investors make better decisions. Not everyone likes to work in a team but, you don’t have to be a member of an Angel group to access some of these resources.

For those who would be angels

However you choose to become an early-stage investor, know that there is a lot more to it than it looks like from the outside and most of your investments are likely to lose all your money. Follow the 24 hour approach and that percentage is likely to go way up. So be sure you can afford that spray-and-pray strategy before you start because whatever strategy you choose, it is only going to work if you can play it through in full.

In the end, I guess there is always the test of walking-the-walk. Does Y Combinator make its investment decisions within 24 hours? Clearly not as some applicants wait months to learn if they have been accepted. So, if that’s the case and Paul isn’t following his own advice, what is the real intent of spreading the word of speed, or, as Paul supposes, is it simply that Y Combinator is imprinted with an obsolete model of risk?

Jordan Green is an internationally sought after thought leader in early-stage investing. Founder of Melbourne Angels, co-founder and chairman of the Australian Association of Angel Investors and Case Manager with Commercialisation Australia.

{kind=link}