QuicklyPay.it (ACT) – 2014 SMART 100

This SMART 100 profile and the information it contains is a duplication of content submitted by the applicant during the entry process. As a function of entry, applicants were required to declare that all details are factually correct, do not infringe on another’s intellectual property and are not unlawful, threatening, defamatory, invasive of privacy, obscene, or otherwise objectionable. Some profiles have been edited for reasons of space and clarity.

1. THE BEGINNING

This innovation came to life when…

My co-founder and I were having dinner out with some mates, and had to split the bill. EFTPOS minimums, and ‘no split bills’ are standard, so one person paid for everything.

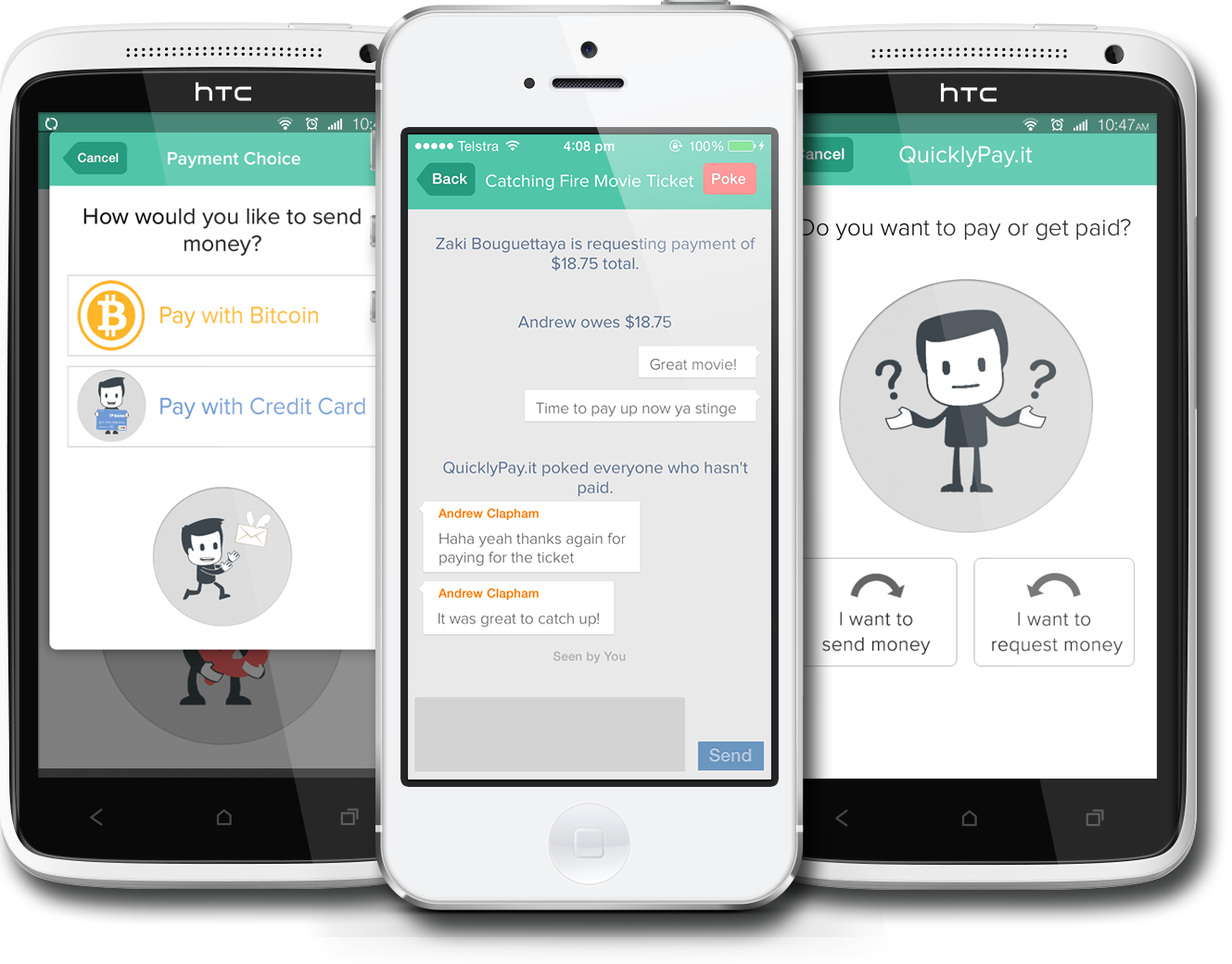

The real pain began for them with reminding friends to pay them back. Phone numbers, then BSBs with account numbers were exchanged. We saw the pain, and have built the solution: an app called QuicklyPay.it. It was launched January 2014.

2. WHAT & HOW

The purpose of this innovation is to…

Solve the social problems of payments between friends and groups of friends.

It does this by…

It does this by providing an informal chat around each payment/request, with the ability to actually pay, inside the chat. Everyone can see who has paid, and who hasn’t, and discuss why the hot water bill is so high this time, for example.

3. PURPOSE & BENEFITS

This innovation improves on what came before because…

An informal group chat provides accountability and social context around a payment that otherwise didn’t exist or had to fit inside an 18 character reference on a bank transfer which can take a few days to arrive.

Its various benefits to the customer/end-user include…

Providing a socially acceptable means to remind friends of cash owed, track who hasn’t paid, as well as send payments without dealing with the exchange of financial details.

4. COMPETITIVE LANDSCAPE

In the past, this problem was solved by…

Friends actively reminding others to pay them back, or exchanging cash in person.

Its predecessors/competitors include…

Bank transfers, Kaching, cash in person as well as the awkward reminder calls and texts.

5. TARGET MARKET

It is made for…

It is made for smartphone users with an Australian bank account or a credit card, who share costs with friends, who pay for concert/movie tickets for the group, who are house mates, or who go to restaurants.

It is available for sale through…

Free download on iPhone and Android, check it out here.

Our marketing strategy is to…

Secure partnerships with use-case relevant businesses (event ticket vendors, cinema chains, restaurants, property managers). Our long term growth strategy is through the organic spread of the app through groups of friends splitting bills with other friends.

Our initial user base was established through incentivising users to invite their friends, combined with Facebook mobile app advertising.

Your Turn — VOTE!

The Readers’ Choice Index was created to provide an opportunity for Anthill readers to vote on SMART 100 applications, in one of three ways:

- Tweet it: Top left of each page (3 points)

- Trigger a Reaction: Facebook ‘Like’, etc (2 points)

- Leave a Comment: Anonymous comments excluded (1 points)

We’ll use your vote to create the 2014 SMART 100 Readers’ Choice Index.

FINE PRINT

This SMART 100 profile and the information it contains is a duplication of content submitted by the applicant during the entry process. As a function of entry, applicants were required to declare that all details are factually correct, do not infringe on another’s intellectual property and are not unlawful, threatening, defamatory, invasive of privacy, obscene, or otherwise objectionable. Some profiles have been edited for reasons of space and clarity.

![Marketlend [SMART 100, 2016]](https://anthillonline.com/wp-content/uploads/2016/04/MarketLend.png)

![Data Creative [SMART 100, 2016]](https://anthillonline.com/wp-content/uploads/2016/04/DATACREATIVE.png)